Quantbase

Strategies

FAQ

Become a partner

Sign in

Get started

Quantbase Insights

Collection of deep-dive posts from our investment team explaining the philosophies behind our funds

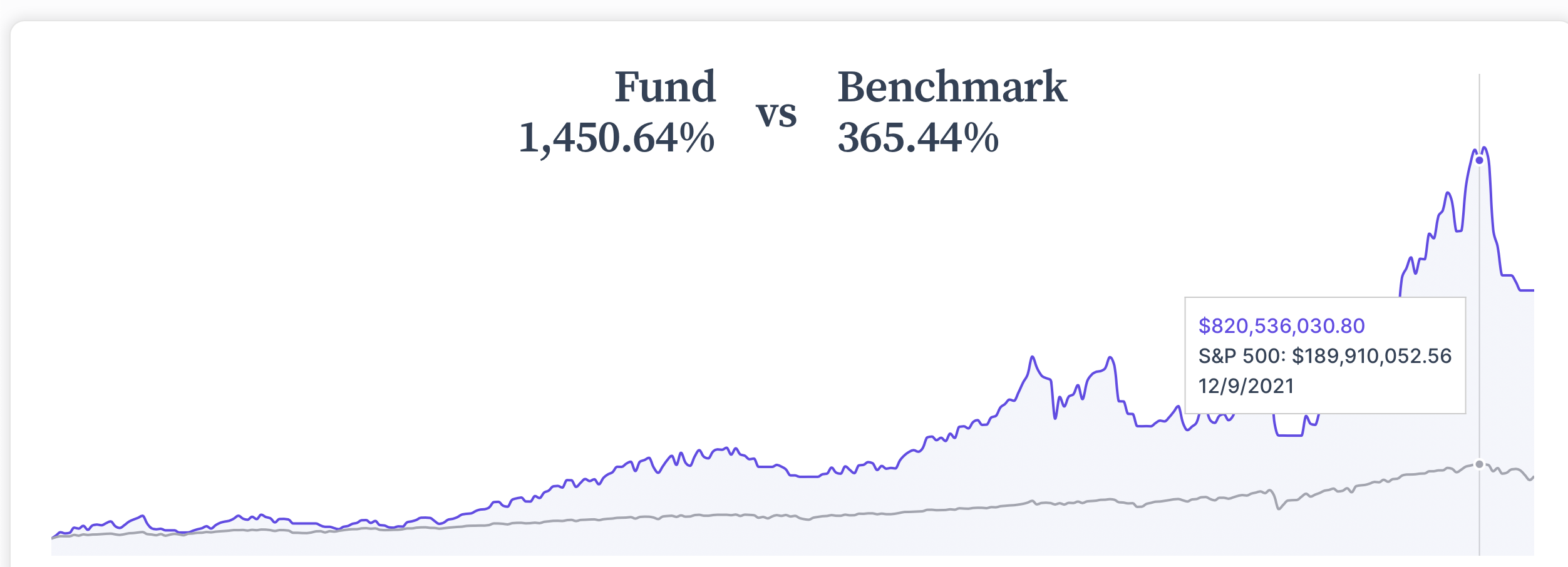

How to Make Money in a Bear Market. Part 1.

It's about buying what others are afraid to. Backtested to 1974 in the research paper this strategy is based on, through 8 crisis events

How Quants Think About Risk

A framework for high-risk investing

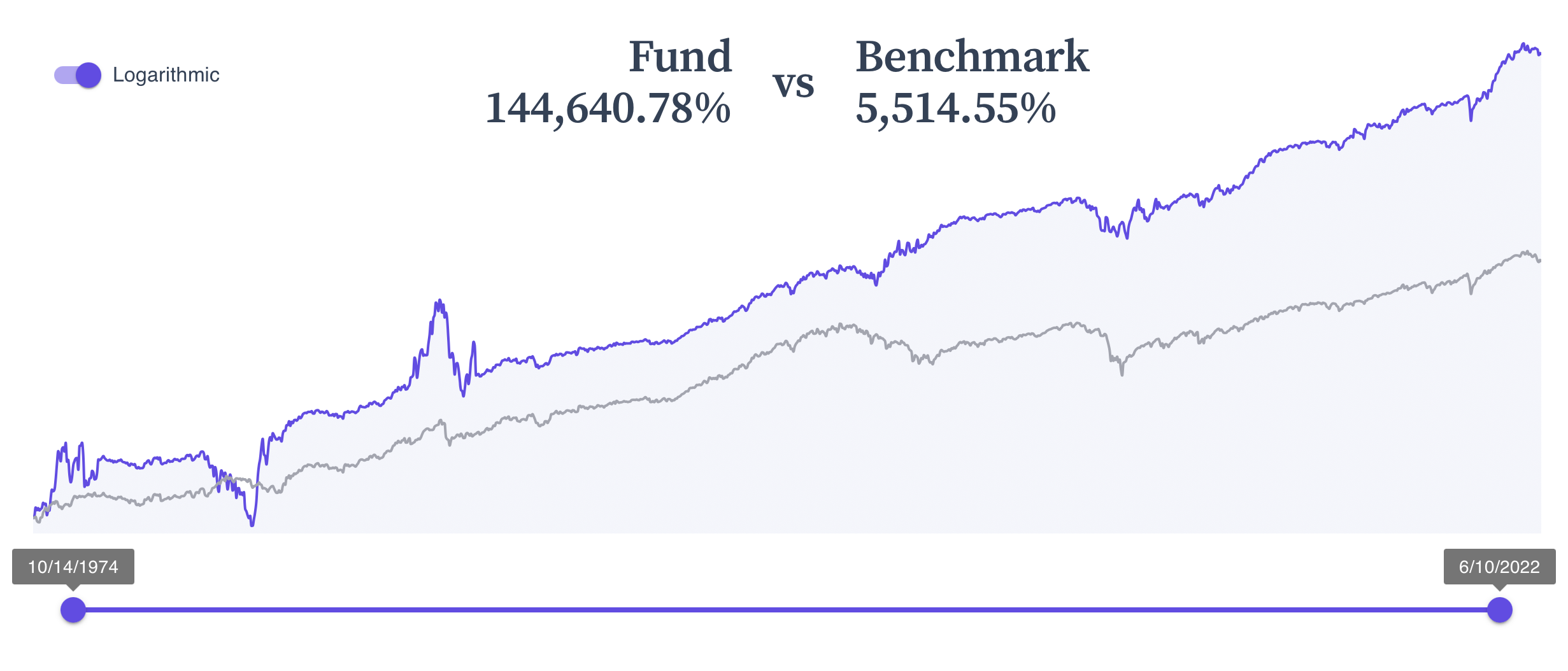

Rules-Based Strategies - The Longest Track Records of Outperformance Ever

Testing investment performance back to October 1928

Quantbase Content Library

Collection of short articles explaining common terms important to understanding investing on Quantbase

The first standardized definition of risk was proposed by Harry Markowitz in his Nobel Peace-Prize winning Modern Portfolio Theory (MPT). MPT divided the returns of any asset into two components - mean returns, and the volatility of those returns. Every asset has those two components. The optimal investment would attempt to choose an asset (or portfolio of assets) that maximizes its returns for a given level of volatility.

There are several metrics that assess the amount of risk you are taking on for a unit of expected return, but one that is frequently used is the Sharpe ratio: Sharpe Ratio = (Expected Returns)/(Expected Volatility). An intuitive way we think about investment risk is by maintaining the Sharpe ratio and increasing both the numerator and denominator. For example, instead of having a Sharpe ratio of 1 in which there is a 10% expected volatility and 10% expected return, keep the Sharpe ratio at 1, but increase expected volatility to 50% and expected return to 50%. That way, you are increasing your risk, but are also increasing your potential reward.

Useful?

Quants are executors of trading strategies that fall under the umbrella of quantitative trading - using computer models and algorithms to predict and capitalize on trading opportunities, often based on historical data and economic/financial insights. Some of the duties of a quant include researching trading strategies, developing algorithms, backtesting using historical data, and implementing strategies with live securities. Quants usually have expertise in finance, mathematics, and computer programming, and are often more willing and familiar with taking greater financial risk than fundamental investors.

Useful?

Beta is a measure of the volatility of an asset or a portfolio in comparison to the broader market (usually the S&P 500). Stocks with betas above 1.0 are considered more volatile than the S&P 500, and stocks with a beta less than 1.0 are considered less volatile than the S&P 500. Since beta is calculated using the covariance of the security’s returns to the overall market, a negative beta means that the market and the security have an inverse relationship (when the market goes up, the security goes down, and vice versa). Beta is often used by investors to judge the amount of risk a stock has; if the beta is less volatile than the market, then there is less risk but also a lower potential for return.

Useful?

Quantitative investing is an investment approach that utilizes advanced mathematical/statistical modeling, algorithms, and data analysis to generate trading strategies. Quantitative investing relies on backtesting algorithms with historical data on a stock’s price, volume, momentum, etc. This investing strategy is particularly useful for creating trigger levels, identifying enter/exit points, quantifying risk, and calculating expected returns. Nobel Prize winner Harry Markowitz is largely credited with popularizing quantitative investment by quantifying the benefits of diversification in Modern Portfolio Theory. In laymans' terms, quant investing is building a portfolio of stocks using research on math and data as well as macroscopic financial knowledge, not based on individual company-level research. Some of the most lucrative hedge funds (including the top performer in history) have been quant funds.

Useful?

Fundamental investing is a type of investing that is the main other style compared to quant investing, and is often the type of investing most people are familiar with. It involves investing in companies based on their fundamentals, meaning doing company/team-level research, talking to companies’ executives to get an idea of the business, and reading company investment memos. Fundamental analysts will use financial information like a company’s revenues, earnings, future growth, and dividends to make their decisions.

Useful?

When investing, traders will often utilize various combinations of economic, fundamental, and statistical factors to make better-informed decisions. Common examples of factors include macroeconomic factors, such as the rate of inflation, GDP, unemployment rate; statistical factors like momentum, volatility, and covariance; and financial factors, such as market capitalization, growth, and risk. One widely known multi-factor model is the Fama and French three-factor model, which uses the size of firms, book-to-market values, and excess return on the market to determine a company’s expected returns.

Useful?

Signals in investing are events or conditions that are set by a trader as an alert for taking an action on an investment. For example, an investor could set a buy signal if Stock X falls in price by $100. If Stock X ever fell $100, the brokerage service would automatically purchase Stock X for the investor. Signals do not have to be for just related to price; quants will often create funds using trigger signals that will cycle a fund in-and-out of a stock if they hit a certain level of volatility or momentum that the quant deems favorable. In essence, signals are used to help ensure that money is being managed to an investor’s desire without the investor having to be constantly monitoring the market.

Useful?

The Sharpe Ratio is the average return earned in excess of the risk-free rate per unit of volatility or total risk. In essence, the Sharpe Ratio helps discern the reward from a given amount of risk. The Sharpe Ratio, developed by William F. Sharpe has many applications and was used in Modern Portfolio Theory to explain how diversification decreases portfolio risk without sacrificing return. If an analysis ever yields a negative sharpe ratio, it means that the risk-free rate is greater than the return, or the portfolio is experiencing negative returns. A “good” Sharpe Ratio falls between 0.75 - 1.0, while a great Sharpe Ratio (which is quite rare) is above 1.0.

Useful?

A market downturn refers to a period in which a market declines. However, keep in mind that market downturns are not the same thing as market recessions. A recession refers to an extended period of time (usually two fiscal quarters) of market decline, while a downturn is a much shorter and less defined period. For example, as of mid-July 2022, the market is on a current downturn as security prices are falling, but not in a recession since two fiscal quarters of contraction have not yet occured.

Useful?

A drawdown is how much an investment or portfolio is down from its peak at a given moment in time. For example, if a portfolio peaked at $1,000,000 over the past 5 years but is now down to $500,000, the drawdown would be 50% over that time period. Drawdown demonstrates the risks of volatility and is used by analysts and quants to make more informed decisions about stocks, especially when looking at historical data or past trading performance.

Useful?

Dollar-cost averaging is an investment strategy proposed by Benjamin Graham that integrates value investing principles into algorithmic trading. The dollar-cost averaging strategy is when an investor puts the same amount of money in securities over a predetermined interval of time (usually monthly or quarterly). The idea behind the dollar-cost averaging strategy is that an investor will be able to take advantage of market downturn by being able to buy more shares when the market is lower compared to when it is high. An alternative strategy to DCA is buying a fixed number of shares each period, but that would not allow the investor to utilize the cyclical nature of markets as much as DCA. The main advantage of DCA is that investors do not have to worry about making day-to-day decisions on their stocks and can instead let DCA generate returns.

Useful?

Backtesting is the general method to assess the historical success of a strategy or model. The underlying assumption with backtesting is that if a strategy worked well in the past, then that strategy is likely to perform well in the future. When backtesting is conducted, it is often centered around a specific time period had similar financial or geopolitical factors affecting the economy to allow for more accurate predictions. The data is then alternatively tested on other similar time periods to validate the strategy’s results.

Useful?

A hedge fund is an actively managed investment pool that is operated by an elite group of investors and quants who attempt to provide exceptional returns for their clients. Hedge funds typically specialize in risky investment strategies or asset classes, and thus charge higher fees than conventional investment funds. Historically, hedge funds were celebrated for their outstanding performance relative to the market in the 1990s and early 2000s, but many have underperformed since the financial crisis of 2008.

Useful?

Financial Independence, Retire Early (FIRE) is a financial movement characterized by spending frugality and an extreme emphasis on savings and investment. FIRE proponents will often save up to 70% of their annual income to retire early and live off small 3-4% yearly withdrawals. The FIRE movement has been largely embraced by millennials, who aim to retire once their total savings hit $1 million. While FIRE is most feasible for those making 6 figures and up, it does not diminish the importance of saving money early to ensure an easy retirement or the opportunity to work at something you love rather than something you have to do.

Useful?

An aggressive/high risk strategy seeks to increase the potential for returns by taking on a higher degree of risk. This type of strategy would likely have a large portion of investment in stocks from growth industries like technology and perhaps newer asset classes like cryptocurrency. Within the portfolio, the investor may try to mitigate risk by diversifying the high-risk investments or may try to increase upside by leveraging certain assets. Aggressive investment strategies require more active management rather than the “buy-and-hold” strategy. Over the past couple years, there has been significant pushback against active investing strategies as investors have pulled their assets out of hedge funds and allocated their money towards passive managers.

Useful?

Hedging is the process of reducing the risk and overall impact of adverse price movements in an asset by taking an opposite position in a related security. However, while hedging reduces risk, it also limits the return potential as the opposite position will likely go down if the initial asset goes up. Hedging is often done through diversification or by purchasing derivatives of a security such as options, swaps, or futures.

For example, if Bill buys 10 shares of Stock X at $100 per share, he could hedge his investment by buying a put option with a strike price of $80 expiring in one year. That means Bill has the option to sell Stock X at $80 anytime the following year. That way, if the price of stock X falls to $60, Bill can sell it for $80 and cut his losses by $20 per share as opposed to the $40 per share he would have lost without the option.

Useful?

Bonds are essential to many portfolios because they offer long-term stability and safe cash flows that help mitigate the impact of a stock market crash. The main types of bonds that are popular in the US include US Treasury bonds, corporate bonds, mortgage bonds, high yield bonds, municipal bonds, and many others. US Treasury bonds are considered one of the safest investments in the world and are considered risk free because investors are essentially betting on the survival of the American economy. Corporate bonds, on the other hand, have credit risk and should therefore be analyzed on the basis of a company’s projected growth and cash flow. Buying corporate bonds from long-established and well-run corporations are the safest option, but may minimize return. Agencies like the Standard & Poor’s provide ratings on corporate bonds to help investors gauge the issuer’s ability to make timely interest and municipal payments.

If you have seen The Big Short, you will remember how the financial crisis of 2008 resulted in a massive crash in mortgage bonds and made a few select individuals who shorted massive amounts of mortgage bonds a large sum of money. Mortgage bonds have risk associated with the probability that underlying borrowers will refinance their mortgages as interest rates change. Finally, with all the other types of bonds, it is important to analyze the yield of these bonds relative to US Treasuries and corporate bonds to understand their potential return and associated risk.

Useful?

The main difference between short and long-term bonds is that long-term bonds are more sensitive to changes in interest rate changes as long-term bonds have greater duration compared to short-term bonds which have fewer coupon payments remaining. Bond prices are inversely related to interest rates, and with long-term bonds, there is a greater probability that interest rates will change. Therefore, if the Federal Reserve decides to increase interest rates because of an economic downturn, a long-term bond’s price will fall.

Useful?

The Treynor ratio is another ratio that expresses the amount of excess return generated for each unit of risk taken on by a portfolio. Mathematically, the Treynor ratio is the portfolio’s excess return divided by the beta of the portfolio. A high Treynor ratio means that the portfolio is a more suitable investment. The Treynor ratio is similar to the Sharpe ratio, but the key difference is that the Sharpe ratio uses a portfolio’s standard deviation to adjust the portfolio’s returns.

Useful?